With Expert, you have until 1 March 2027 to file. Let us handle it.

Missed the tax deadline?

No problem. With Taxfix Expert, your tax deadline is extended to 1 March 2027. Our independent tax advisors take care of everything, so you can sit back and relax.

Now available: Taxfix for the Self-employed!

Germany's most popular tax app: + 10 million tax returns submitted

Why Taxfix is right for you

Simple. Secure. Worth it. That’s how you file your taxes with Taxfix.

Simply simple

Step by step to a finished tax return – no tax jargon, no prior knowledge, no stress.

Expert-built

Our app was developed by real tax professionals – for a safe and accurate submission.

Avg. refund: €1,240

We make sure you get what you’re entitled to – with all deductions, allowances, and expenses applied.

In safe hands

Your data is fully protected – with state-of-the-art encryption and secure transmission.

Extend your deadline with Expert

Missed the tax deadline? Let one of our independent tax advisors handle your taxes and buy yourself more time.

Start nowTo date, more than 10 million tax returns have been submitted through Taxfix, leading to more than € 5 billion in refunds.

Tax experts work at Taxfix.

Employees counts Taxfix currently.

| Supported | |

|---|---|

| Employee | |

| Families | |

| Students | |

| Pensioners | |

| Landlord (VAT-exempt) | |

| Small business owners who fall under “Kleinunternehmer” regulations | |

| VAT-liable self-employed individuals | |

| Civil servant pensions / Income from forestry and agriculture / Year-round residence abroad / Residences in two countries simultaneously / Foreign income |

Supported tax cases

We are constantly working to expand our offering and make our services accessible to more people. Here you will find a list of currently supported and not yet available tax cases. Now also available for self-employed.

How much does Taxfix cost?

You can use Taxfix from €39.99 or €99.99: Choose exactly the solution that suits you and your needs. Find our full pricing details on our costs page

Expert

Your personal point of contact

Your tax advice tailored to you and your case

Experts by your side

Contact your expert anytime

Error-free instead of paying extra

Have your taxes reviewed risk-free by licensed experts

Don't leave money on the table

Experts get you what you're owed

Extended filing deadline

March 1st 2027

Basic

Clear & fast

You handle everything step by step

See your refund in advance

First estimate, without guarantee

Zeit sparen

Werte aus dem Vorjahr übernehmen

Start

Calculate your refund for free

Find out in minutes what the tax office owes you.

File directly

Happy with the amount? File directly with Basic

Fits you perfectly

Like to do it yourself? Prefer to sit back? Either way – we’ve got you.

Your taxes, done with Expert

Minimal effort, optimal return. Independent tax experts prepare your return for you. After answering just a few questions, you'll receive a personalized task list to provide your documents. No appointments or time-consuming searches. 100% digital and at a fair price.

Start nowFile your taxes yourself

Done in minutes, not months. Snap a photo of your income statement, answer a few simple questions, and instantly see how much you’ll get back. Free to try – you only pay when you submit.

Start nowThe tax platform now also freelancers

Whether you're VAT-registered or filing once a year, Taxfix for Self-Employed brings your tax workflow into one place — with plain-language guidance and built-in checks.

Start for freeAre you self-employed?

Whether a small business owner or VAT-liable freelancer , we’ve got you covered!

| ELSTER | Taxfix Basic | Taxfix Expert | |

|---|---|---|---|

| Official ELSTER interface | |||

| Fully digital process from start to finish | |||

| Easy to understand – no tax jargon | |||

| Save and categorise documents to maximise your refund | |||

| Additional tax tips and instructions | |||

| Process and guidance in English | |||

| Matched with a tax expert in seconds – no searching required | |||

| Tax experts optimise your return | |||

| Expert chat: Get answers to your questions – even after submission | |||

| Automatic updates on your tax return status | |||

| Calculate refund for free | |||

| Price | Free | From €39.99 | from €99.99 |

Why pay for Taxfix, if ELSTER is free?

With Germany’s most popular mobile tax app, you can save money on your tax return – without stress or tax knowledge. The average refund? €1,240.

Plan smart. Save smarter.

Photograph, categorise, and save your receipts right when you get them. This way, you can save money even more easily on your next tax return.

Start now

Multiple awards!

With Germany's most popular mobile tax app, you can do your tax return in no time.

Elster

Thanks to the API interface to ELSTER, your data will be securely transmitted to the tax office.

Finanztip

The consumer magazine Finanztip recommends Taxfix as tax software for a simple tax return.

Best reviews

More than 255.000 positive reviews with an average rating of 4.6 stars speak for themselves.

Made in Germany

Innovation meets quality. Taxfix is developed and designed in Berlin. By people from all over the world.

Frequently asked questions

With our app developed by tax experts, we successfully help people every year.

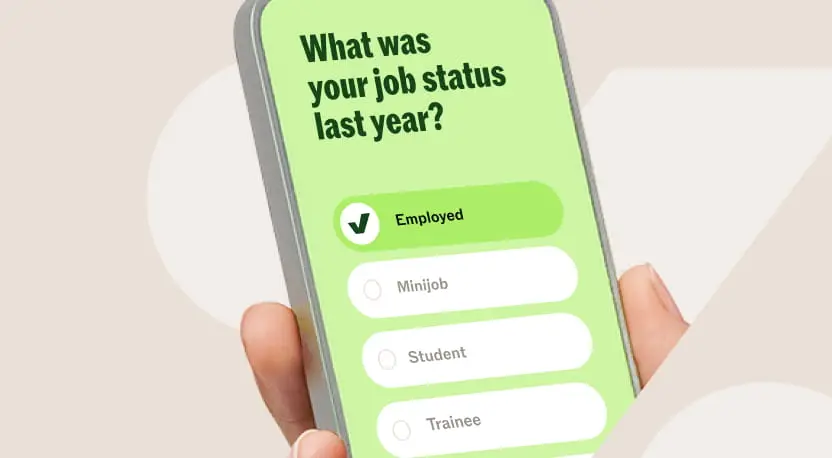

There are two ways to file your tax return with Taxfix: complete the simple question-and-answer process with Basic via app or browser, or have your taxes done by an independent tax advisor using Expert .

If you do your tax return yourself, you can get a free calculation of your estimated refund before submitting to your local tax office via the official ELSTER interface.

Expert: With Expert , independent tax advisors prepare your tax return for you. A personal task list shows you exactly which documents to upload, so your expert can optimise your return. In the end, all you have to do is review and approve your tax return – and you're done!

Basic : After registering via the app or browser, you'll answer around 70 personalised questions. Then, you’ll immediately see an estimate of your potential refund – for free. If you decide to file, we’ll submit your tax return digitally to your local tax office. Once processed, your refund will be transferred directly to your bank account, and you’ll receive your official tax assessment notice.

Download the Taxfix app for free from the Apple App Store, the Google Play Store, or access our site in your web browser. At no extra cost, you can calculate your expected tax refund. Alternatively, you can use Expert and have your tax return done for you by an independent tax advisor. Find the current prices for both services on the Taxfix costs page .

Submitting a tax return is definitely not something you do off the cuff. And when specialized knowledge is required, it’s understandable to be cautious or even feel sceptical.

For questions that require explanation, Taxfix offers info texts and corresponding advice articles or tax tips. These resources will help with general tax questions on specific points, but not with individual tax questions.

Your question not yet included? We have collected the most frequently asked questions and our answers in our Support Center .

Trusted by millions, built for everyone

See why the Taxfix app is Germany’s #1 choice for stress-free tax filing.

Start now for free